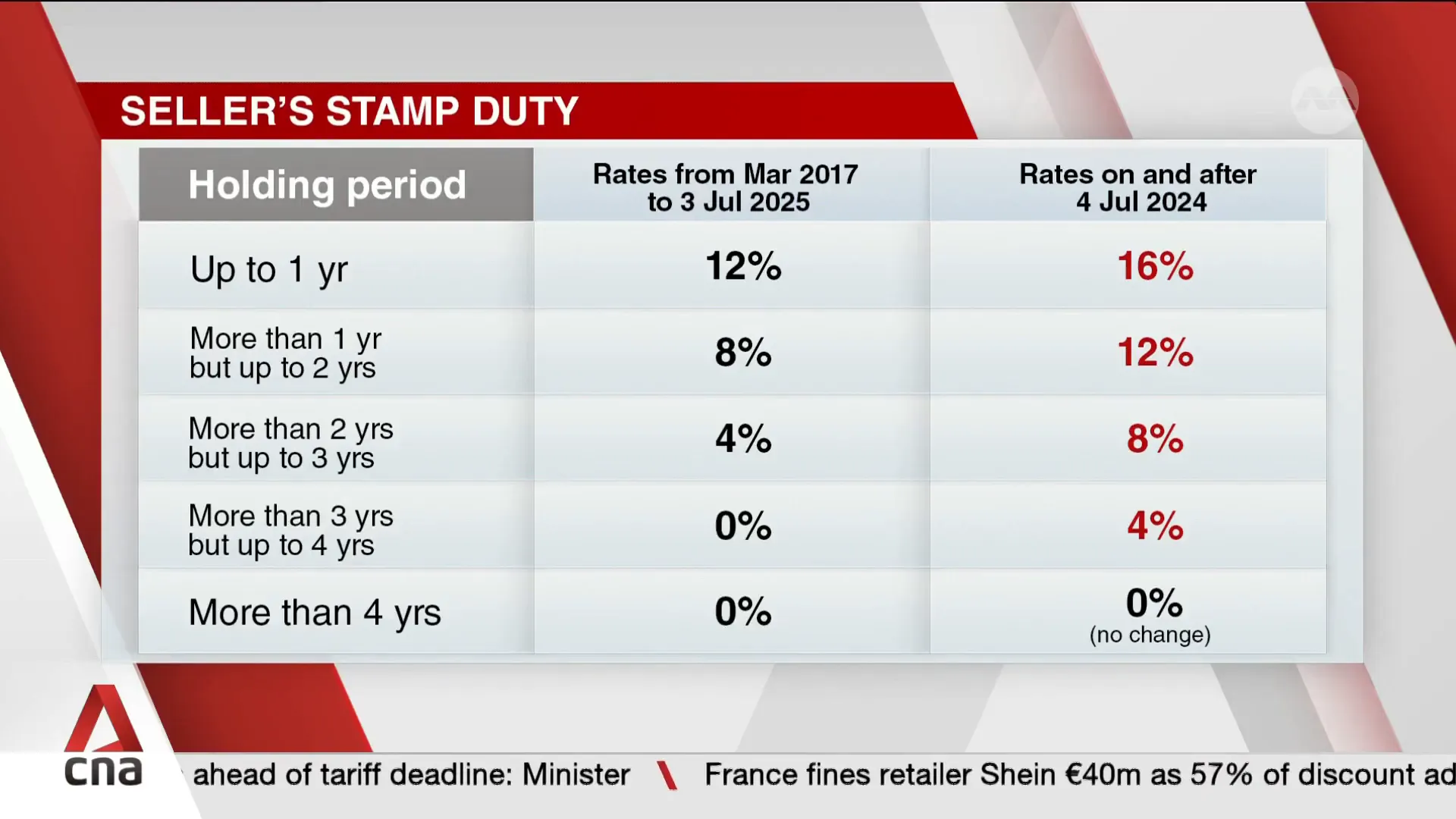

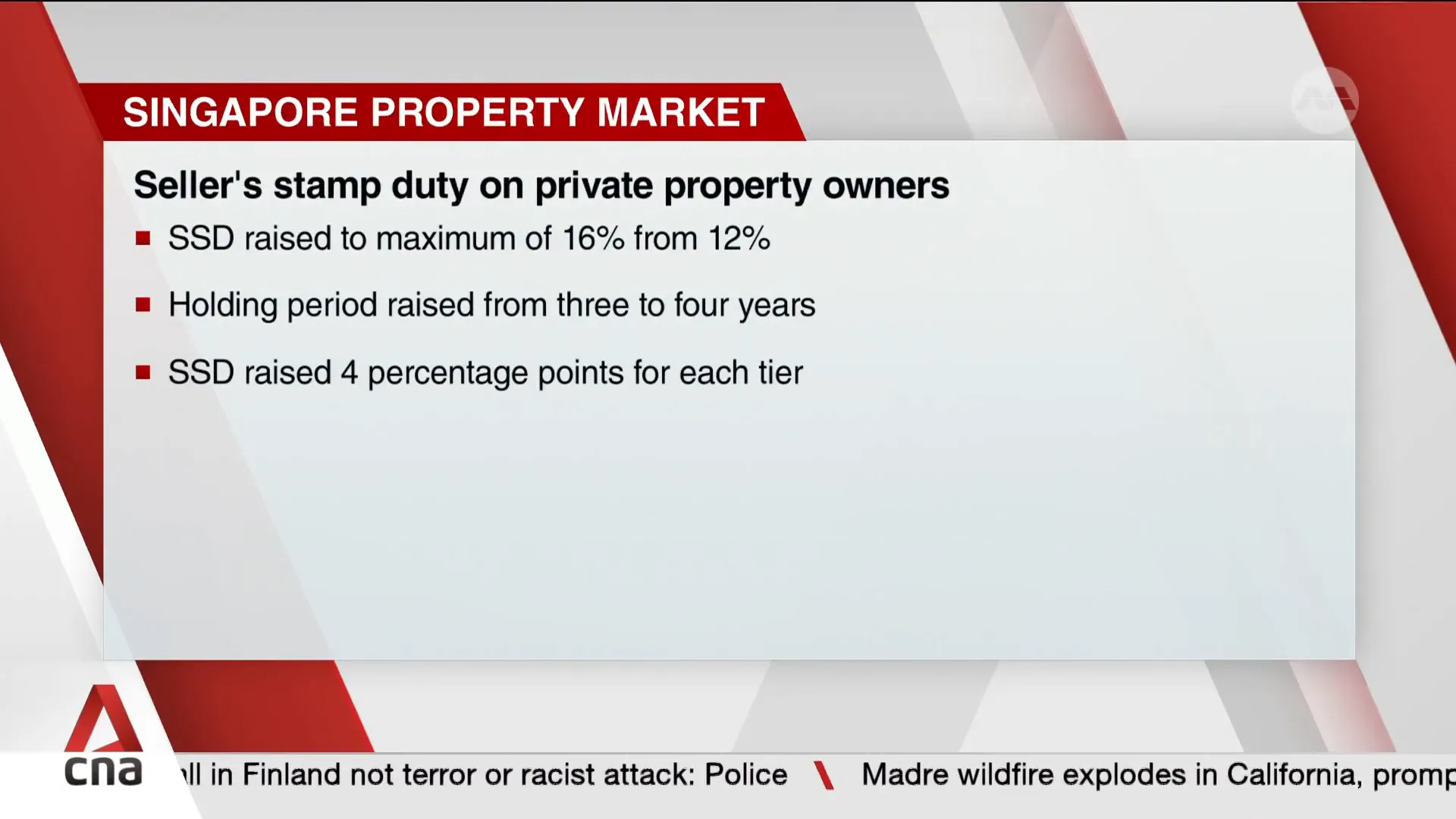

In a significant move aimed at cooling down Singapore’s private property market, the government has announced that private homeowners selling their properties within four years of purchase will now face a seller’s stamp duty (SSD) that applies for a longer period than before.

This change extends the holding period from three years to four years and raises the SSD rates by four percentage points across all holding periods. The announcement, made on July 3, 2024, is part of a broader strategy to curb speculative property flipping, particularly in newly constructed homes that are sold before completion.

To better understand the implications of these new rules, Alan Chong, Executive Director for Research and Consultancy at Savills Singapore, shares his expert insights on the market dynamics, the rationale behind the policy, and the potential ripple effects on both private and public housing prices.

This article explores the key details of the seller stamp duty increase to 16%, its impact on property flipping, and what Singaporean homeowners and investors can expect in the months ahead.

Table of Contents: Seller Stamp Duty Increases to 16%

- 📈 What Are the New Seller Stamp Duty Rules?

- 🏠 Understanding the Rise in Property Flipping

- 👥 Who Are the Main Players Behind Property Flipping?

- 📉 What Impact Will the New SSD Rules Have on the Property Market?

- 🏢 How Will the Changes Affect Public Housing and HDB Prices?

- 📊 Forecasting Singapore’s Property Market for the Rest of 2024

- 🏢 What About Collective Sales and Enbloc Market Dynamics?

- 🔍 Frequently Asked Questions (FAQ)

- 🔑 Conclusion: What Homeowners and Investors Need to Know

📈 What Are the New Seller Stamp Duty Rules?

Starting from July 3, 2024, private property owners in Singapore who sell their properties within four years of purchase will be subject to a seller’s stamp duty.

This is a tightening of the previous rule, where SSD applied if the property was sold within three years. Alongside this extension, the actual rates of SSD have been increased by four percentage points for every holding period bracket.

To put the changes in perspective:

- Previously, selling a property within one year of purchase attracted a 12% SSD on the actual selling price or market value.

- Under the new rules, this rate has increased to 16% for properties sold within one year.

- For sales made within the second and third years, the SSD rates have also risen correspondingly.

- Properties held for more than four years are exempt from SSD altogether.

These rules apply exclusively to private residential properties and do not affect public housing (HDB flats). The government’s stated objective is to discourage short-term speculative buying and selling, which has been seen as a destabilising factor in the property market.

🏠 Understanding the Rise in Property Flipping

Alan Chong explains that the government’s decision comes in response to a sharp increase in property flipping activities. Flipping refers to the practice of purchasing a property and quickly reselling it for a profit, often within a few months or even years.

Between 2017 and 2019, private residential prices in Singapore remained relatively flat. However, after the COVID-19 pandemic, the market saw a significant upward “step function” or price jump due to renewed demand and new property launches.

This price gap created an opportunity for homeowners who purchased properties during the flat period to realise substantial profits by reselling during the price surge.

Because of this windfall, many owners were motivated to flip their properties within a short period, contributing to increased transaction volumes involving short holding periods. This trend was especially prominent in new launches, which are often sold before completion, sometimes even years ahead.

👥 Who Are the Main Players Behind Property Flipping?

Contrary to popular assumptions, most of those involved in flipping private properties are Singaporean locals rather than foreigners. Alan highlights that Singaporeans constitute the majority of buyers for new launches, which are the primary sites of flipping activity.

Here’s why flipping has been feasible despite the holding period requirements:

- Developers typically receive permission to launch a project about 15 to 18 months after acquiring the land.

- Completion of the property usually takes several years following the launch.

- During this time, new projects are continually launched, often at progressively higher prices due to market appreciation.

- Buyers who purchased early benefit from price increases before completion, enabling them to flip the property before taking physical possession.

This cycle creates a window where owners can realise capital gains without physically occupying the property, driving the short-term speculative market.

📉 What Impact Will the New SSD Rules Have on the Property Market?

Alan Chong believes the new seller stamp duty rules will primarily discourage speculative buyers and flippers. For genuine homeowners and long-term investors, the impact will be minimal as they tend to hold onto their properties beyond the four-year SSD period.

Specifically, the increased SSD and longer holding period will make it harder for flippers to justify purchases aimed at short-term profits. Real estate agents and marketers who previously promoted quick-flip opportunities will need to adjust their narratives, as the financial incentives for flipping diminish.

Consequently, the private property market may see a slowdown in transaction volumes related to quick resales, leading to a more stable and sustainable growth trajectory.

🏢 How Will the Changes Affect Public Housing and HDB Prices?

The seller stamp duty increases are targeted at private residential properties and do not directly apply to public housing (HDB flats). However, the policy could have indirect effects on the HDB resale market.

Historically, some homeowners who profited from flipping private properties used their gains to upgrade to HDB flats in better locations or with higher prices. By curbing flipping profits, the new SSD rules may reduce the number of buyers moving from private properties back to the HDB market, potentially slowing demand for public housing.

Alan explains that if the private market prices remain relatively stable or flat, the influx of buyers into the HDB resale market may be delayed. However, if private property prices continue to rise rapidly, the SSD could indirectly contribute to upward pressure on HDB resale prices by limiting the supply of buyers able to upgrade.

Therefore, the new SSD rules represent an “indirect attack” on rising HDB prices by influencing the flow of capital between the private and public housing sectors.

📊 Forecasting Singapore’s Property Market for the Rest of 2025

Looking ahead, Alan expects private residential prices to increase by about 7% year-on-year in 2025, while HDB resale prices may see a 5-6% rise. These projections take into account the new SSD rules, which are likely to have a more pronounced effect towards the end of the year and beyond.

The gradual implementation of these policies gives the market time to adjust, with the most significant impact expected as current holding periods expire and buyers reconsider short-term speculative strategies.

🏢 What About Collective Sales and Enbloc Market Dynamics?

Another segment of the property market affected by the broader economic environment is the collective sale or enbloc market, where multiple owners sell their units to developers for redevelopment.

Alan notes that collective sales are currently facing challenges unrelated to the SSD changes. Sellers are asking for prices that developers find too high, making government land sales more attractive due to better yields and more manageable project sizes. As a result, developers are less inclined to pursue large collective sales projects that require significant upfront investment and risk.

This dynamic means that collective sales activity remains subdued, and the new SSD rules are unlikely to have a significant direct impact on this market segment in the near term.

🔍 Frequently Asked Questions (FAQ)

What is the seller stamp duty (SSD) increase to 16% about?

The government has increased the SSD rate to 16% for properties sold within one year of purchase, up from the previous 12%. The holding period for SSD liability has also been extended from three to four years, applying to all private residential properties bought from July 4, 2025, onward.

Who does the new seller stamp duty apply to?

The new SSD rules apply to private residential property owners in Singapore who sell their properties within four years of purchase. It does not apply to public housing (HDB flats) owners.

Why did the government introduce these changes?

The changes aim to curb speculative property flipping, which has increased sharply in recent years, especially for new launches sold before completion. The goal is to stabilise the property market and reduce short-term price volatility.

How will the SSD increase affect property flipping?

The higher SSD rates and longer holding period will reduce the profitability of flipping properties quickly. This is expected to discourage short-term speculative buying and selling, leading to a more stable market.

Will these changes affect HDB resale prices?

Indirectly, yes. Reduced profits from private property flipping may slow the flow of buyers upgrading to HDB flats, potentially affecting demand and prices in the HDB resale market.

What is the outlook for Singapore’s property market in 2025?

Private residential prices are expected to rise by around 7% year-on-year, while HDB resale prices may increase by 5-6%. The SSD changes will likely have a more noticeable impact towards the end of the year and beyond.

Are collective sales affected by the new SSD rules?

Collective sales are facing challenges mainly due to pricing and market dynamics rather than the SSD changes. Developers currently prefer government land sales over large collective sale projects due to better yields and manageable project sizes.

🔑 Conclusion: What Homeowners and Investors Need to Know

The increase in seller stamp duty to 16% for properties sold within a year, alongside the extension of the SSD holding period to four years, marks a clear government intent to rein in speculative property flipping in Singapore’s private residential market.

This policy change targets a growing trend where buyers, mostly Singaporean locals, leverage rising prices in new launches to realise quick profits before completion.

For genuine homeowners and long-term investors, the impact will be limited, but speculative buyers will face higher costs and longer holding requirements that reduce the attractiveness of quick flips.

This is expected to bring more stability to the private property market, dampening rapid price surges and volatile transaction volumes.

Additionally, the new rules may indirectly influence public housing prices by slowing down the flow of capital between private and HDB markets.

Homeowners upgrading from private properties to HDB flats may find fewer opportunities to capitalise on short-term gains, potentially easing demand pressure in the HDB resale market.

As Singapore’s property landscape continues to evolve, staying informed about policy changes like the seller stamp duty increase to 16% is crucial for buyers, sellers, and investors alike.

Understanding these dynamics can help market participants make more strategic decisions in a changing regulatory environment.

For those interested in deeper analysis and market updates, following expert insights from property consultants like Alan Chong and trusted real estate agencies will provide valuable guidance in navigating Singapore’s complex property market.

Disclaimer: The information provided here is for general guidance only. PropsBit.com.sg does not endorse or guarantee its suitability or accuracy for your specific situation. Although we strive to ensure the content is accurate and reliable at the time of publication, it should not substitute personalised advice from a qualified professional. We strongly recommend not relying solely on this information for financial, investment, property, or legal decisions, and we disclaim any responsibility for decisions made based on this content.

This website’s information is meant solely for general informational use. PropsBit.com.sg and its authors disclaim all liability and responsibility to any individuals or organisations for any outcomes resulting from the use of this website’s content or the information presented here. PropsBit.com.sg reserves the right to add, remove, or change the website’s content at any time without prior notice.