The Singapore property market experienced a significant slowdown in May 2025, with Singapore New Home Sales reaching their lowest levels this year. Despite the monthly decline, the market showed resilience with year-on-year growth and continued strength in the luxury segment.

New Home Sales Fall to Lowest 2025 Levels Despite Year-on-Year Growth of 40%

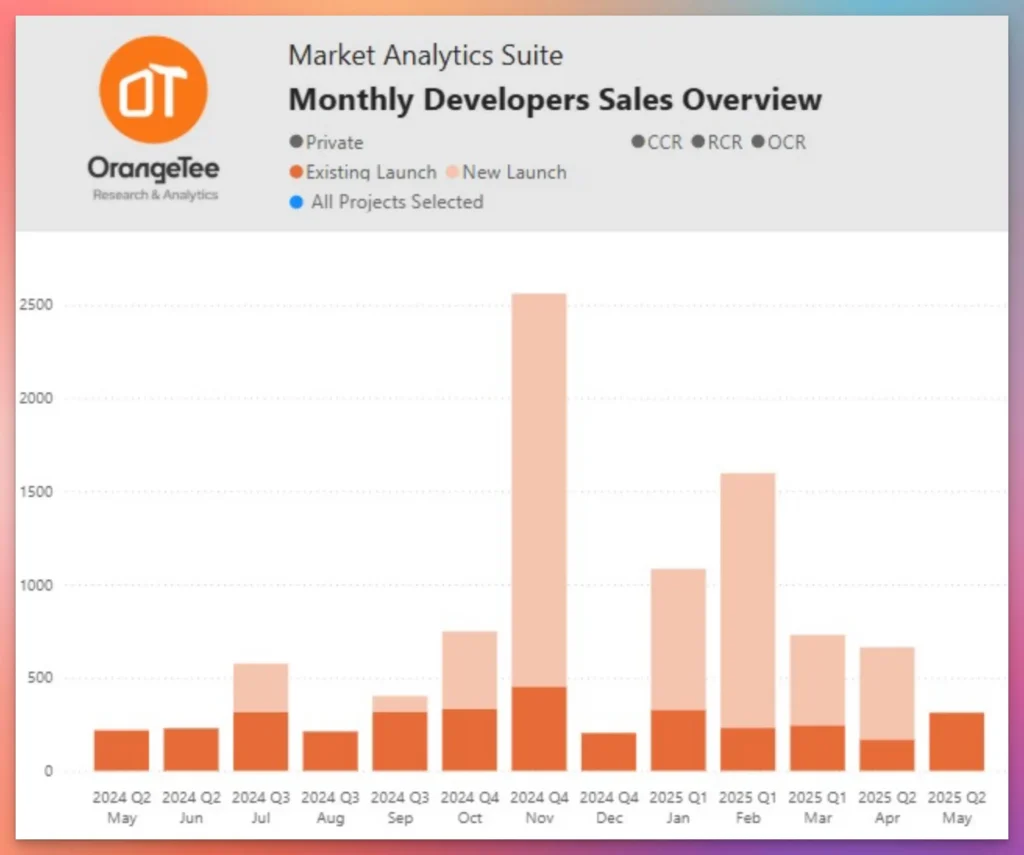

According to the latest data from the Urban Redevelopment Authority (URA), Singapore’s new home sales, specifically the Singapore New Home Sales excluding Executive Condominiums (ECs), dropped dramatically to 312 units in May 2025, representing a substantial 52.9% decline from April’s 663 units. The figures underscore the challenges facing Singapore New Home Sales.

When including ECs, the total sales volume decreased even more sharply by 55.7%, falling from 759 units in April to just 336 units in May.

| Month ……… | Sales Volume . | New Launches |

| (Excl. EC) | (Incl. EC) | (Excl. EC) | (Incl. EC) | |

| May-24 | 223 | 263 | 270 | 270 |

| Dec-24 | 203 | 373 | 20 | 20 |

| Jan-25 | 1,083 | 1,104 | 896 | 896 |

| Feb-25 | 1,597 | 1,626 | 1,694 | 1,694 |

| Mar-25 | 729 | 1,510 | 555 | 1,315 |

| Apr-25 | 663 | 759 | 1,344 | 1,344 |

| May-25 | 312 | 336 | 20 | 20 |

| M-o-M % Change | -52.9% | -55.7% | -98.5% | -98.5% |

| Y-o-Y % Change | 39.9% | 27.8% | -92.6% | -92.6% |

Key Market Performance Indicators May 2025

The absence of new project launches was the primary driver behind May’s subdued sales performance. Additionally, many potential buyers were engaged in election-related activities, further dampening market activity during the month.

Despite the monthly decline, the Singapore property market demonstrated underlying strength with Singapore New Home Sales (excluding ECs) showing impressive year-on-year growth of 39.9%, rising from 223 units in May 2024 to 312 units in May 2025.

Notably, the trend of Singapore New Home Sales highlights how the overall market is responding to economic shifts and buyer sentiment.

Singapore Property Market by Regional Performance

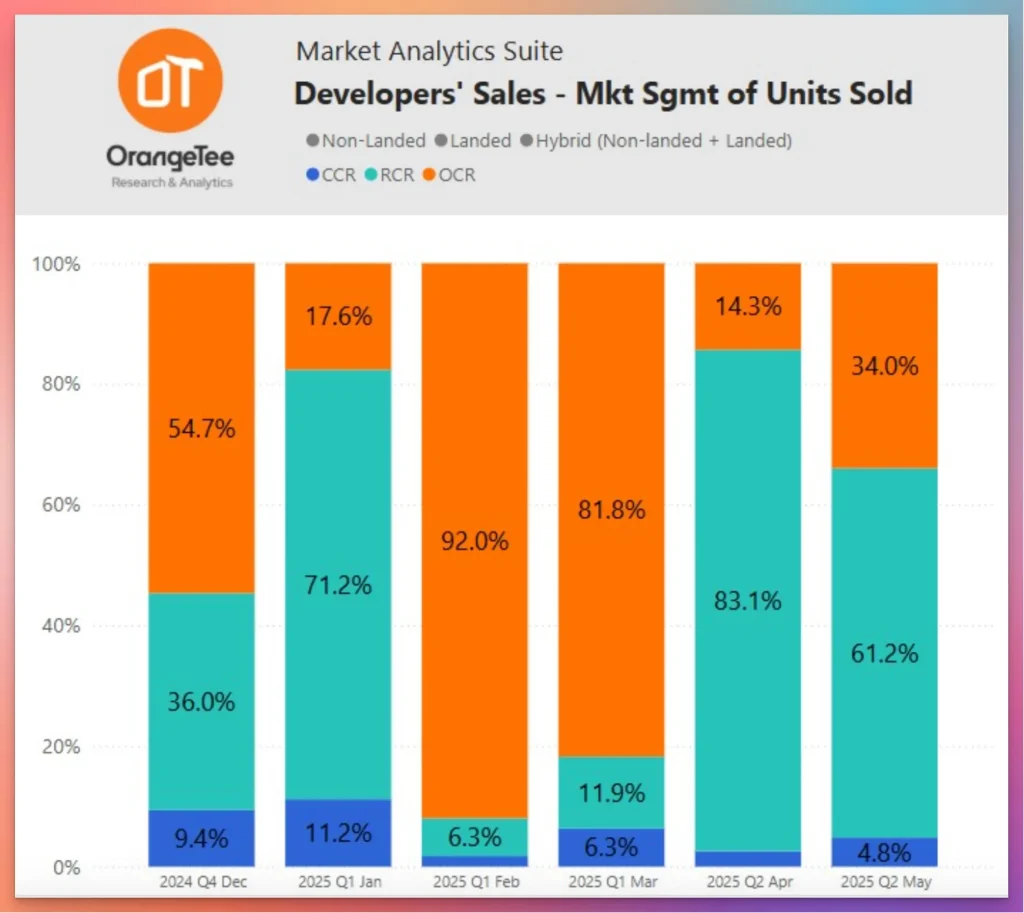

Rest of Central Region Dominates Sales with 61% Market Share

The geographical distribution of new home sales in May 2025 revealed distinct patterns across Singapore’s property regions:

- Rest of Central Region (RCR): 191 units sold, accounting for 61.2% of total transactions

- Outside Central Region (OCR): 106 units sold, representing 34% of total sales

- Core Central Region (CCR): 15 units sold, comprising 4.8% of total transactions

This regional breakdown highlights continued buyer preference for city fringe locations, which offer better value propositions compared to prime central areas while maintaining good connectivity and amenities.

Ultra-Luxury Property Transactions Remain Strong with Record Sales

Premium Segment Defies Market Slowdown

Despite the overall market decline, Singapore’s ultra-luxury property segment demonstrated remarkable resilience in May 2025.

Three non-landed private homes were transacted above S$10 million, matching the previous month’s performance and indicating sustained demand among high-net-worth buyers.

Notable Ultra-Luxury Transactions May 2025:

Record-Breaking Sale: The month’s most significant transaction was a 4,489 square foot unit at the newly launched 21 Anderson project, which sold for S$24 million, establishing a new benchmark for luxury property values.

Premium Gilstead Sales: Two substantial units at 32 Gilstead, measuring 4,209 and 4,219 square feet respectively, were both transacted for S$15.1 million each, demonstrating consistent pricing in the premium segment.

Luxury Market Shows Strong Recovery

The luxury property market, defined as homes priced between S$5 million and S$10 million, experienced significant improvement in May 2025. Nine new non-landed homes in this price range were sold, representing a substantial increase from just two units in April 2025.

These luxury sales were distributed across several prestigious developments, including 21 Anderson, Watten House, Canninghill Piers, Aurea, and Terra Hill, indicating broad-based demand across different luxury projects.

Copyright © OrangeTee & Tie Pte Ltd. All rights reserved

Top-Performing Singapore Property Projects May 2025

Best-Selling Developments Drive Market Activity

In the absence of new launches, existing projects carried the momentum for Singapore’s property market in May 2025:

Leading Projects by Sales Volume:

- One Marina Gardens: 62 units sold

- Bloomsbury Residences: 32 units sold

- The Hill @ One-North: Strong performance in the RCR segment

- Hillock Green: Continued buyer interest in suburban locations

- Grand Dunman: Sustained sales in the eastern region

Other notable performers included Nava Grove, Lentor Mansion, The Orie, and Parktown Residence, demonstrating diversified buyer interest across different price points and locations.

Singapore Property Market Outlook: Second Half 2025 Prospects

Robust Pipeline Expected to Revitalise Market Activity

The Singapore property market is positioned for potential recovery in the second half of 2025, supported by several positive factors:

Upcoming Major Launches:

- Arina East Residences: 107 units in the eastern region

- The Robertson Opus: 348 units in the central area

- The Sen: 347 units adding to the market supply

- Springleaf Residence: 941 units representing significant new inventory

- River Green: 524 units contributing to suburban options

Market Drivers and Challenges

Positive Factors:

- Moderating Interest Rates: Improving affordability for mortgages and potentially attracting investors back to the market

- HDB Upgrader Market: Lower interest rates may enable more HDB flat owners to upgrade to private condominiums

- Strong Fundamentals: Employment stability and steady real wages support buyer confidence

Market Challenges:

- Global Economic Uncertainty: US tariff policies creating trade challenges that may affect buyer sentiment

- Cautious Investment Approach: Some buyers are adopting wait-and-see attitudes due to economic volatility

Historical Context: Singapore Property Performance Analysis

May 2025’s sales performance, while lower than recent months, still outperformed comparable periods without new launches over the past three years. This resilience can be attributed to the more favourable interest rate environment compared to previous years, keeping property purchases more accessible for buyers.

The last time Singapore recorded higher property sales in a month without new launches was June 2022, prior to the implementation of additional cooling measures, highlighting the current market’s relative strength despite challenging conditions.

Singapore Property Investment Implications

Market Positioning for Investors

The current market dynamics present both opportunities and considerations for property investors:

Investment Opportunities:

- Selective Buying: Reduced competition may create better negotiating positions

- Quality Projects: Focus on well-located developments with strong fundamentals

- Luxury Segment: Continued strength in high-end market segments

Risk Considerations:

- Economic Headwinds: Global trade tensions require careful market timing

- Interest Rate Sensitivity: Monitoring monetary policy changes affecting financing costs

| Project Name | Locality | Total No. of Units | Cumulative Units Launched to date | Cumulative Units Sold to date | Sold in the month | Median Price (Spsf) | Take up Rate^ (%) | Sold out status* (%) |

|---|---|---|---|---|---|---|---|---|

| One Marina Gardens | RCR | 937 | 937 | 435 | 62 | $2,975 | 46.4% | 46.4% |

| Bloomsbury Residences | RCR | 358 | 358 | 137 | 32 | $2,506 | 38.3% | 38.3% |

| The Hill @ One-North RCR | RCR | 142 | 142 | 94 | 25 | $2,484 | 66.2% | 66.2% |

| Hillock Green | OCR | 474 | 460 | 434 | 17 | $2,285 | 94.3% | 91.6% |

| Grand Dunman | RCR | 1008 | 1008 | 784 | 15 | $2,524 | 77.8% | 77.8% |

| Nava Grove | RCR | 552 | 552 | 437 | 13 | $2,545 | 79.2% | 79.2% |

| Lentor Mansion | OCR | 533 | 533 | 524 | 11 | $2,194 | 98.3% | 98.3% |

| The Orie RCR | RCR | 777 | 777 | 707 | 10 | $2,631 | 91.0% | 91.0% |

| Parktown Residence | OCR | 1,193 | 1,193 | 1,072 | 10 | $2,410 | 89.9% | 89.9% |

| Hillhaven | OCR | 341 | 341 | 313 | 9 | $2,098 | 91.8% | 91.8% |

^Take-up rate is calculated by dividing the division of cumulative units sold to date by the cumulative units launched to date

*Sold out status is calculated by taking the division of cumulative units sold to date over the total no. of units in the project.

Conclusion: Singapore Property Market Resilience Amid Challenges

Singapore’s property market in May 2025 demonstrated the characteristic resilience that has defined the sector through various economic cycles.

While new home sales experienced their lowest monthly performance of the year, the underlying fundamentals remain sound with strong year-on-year growth and robust luxury market performance.

The anticipated pipeline of new launches in the second half of 2025, combined with moderating interest rates and stable economic conditions, positions the Singapore property market for potential recovery and continued growth.

Investors and homebuyers can expect increased choices and potentially more competitive pricing as new supply enters the market.

The luxury segment’s continued strength, evidenced by multiple ultra-high-value transactions, underscores Singapore’s position as a premier destination for international real estate investment and its appeal to high-net-worth individuals seeking quality property assets in a stable market environment.

Frequently Asked Questions (FAQ)

Q1: Why did Singapore’s new home sales drop so significantly in May 2025?

A: Singapore’s new home sales dropped 52.9% in May 2025, primarily due to the absence of new project launches during the month.

Additionally, many potential buyers were engaged in election-related activities, which further reduced market activity. Despite this monthly decline, sales still showed strong year-on-year growth of 39.9% compared to May 2024.

Q2: How many new homes were sold in Singapore in May 2025?

A: In May 2025, Singapore recorded 312 new home sales excluding Executive Condominiums (ECs), and 336 units including ECs. This represents the lowest monthly sales figure for 2025, down from 663 units (excluding ECs) in April 2025.

Q3: Which Singapore property projects performed best in May 2025?

A: The top-performing projects in May 2025 were:

- One Marina Gardens: 62 units sold

- Bloomsbury Residences: 32 units sold

- Other strong performers included The Hill @ One-North, Hillock Green, Grand Dunman, Nava Grove, Lentor Mansion, The Orie, and Parktown Residence.

Q4: What was the most expensive property sale in Singapore in May 2025?

A: The most expensive property transaction in May 2025 was a 4,489 square foot unit at 21 Anderson, which sold for S$24 million. This was followed by two units at 32 Gilstead, each measuring over 4,200 square feet and selling for S$15.1 million each.

Q5: How did different regions of Singapore perform in the property market?

A: Regional performance in May 2025 showed:

- Rest of Central Region (RCR): 191 units (61.2% of total sales)

- Outside Central Region (OCR): 106 units (34% of total sales)

- Core Central Region (CCR): 15 units (4.8% of total sales)

The RCR dominated sales due to attractive pricing and good locations.

Q6: Is the Singapore luxury property market still strong?

A: Yes, the luxury property market remained robust in May 2025. Three properties sold above S$10 million, and nine homes priced between S$5-10 million were transacted, compared to only two in April 2025. This demonstrates continued strong demand in the premium segment.

Q7: What new property launches are expected in Singapore for the rest of 2025?

A: Several major launches are expected in the second half of 2025:

- Arina East Residences: 107 units

- The Robertson Opus: 348 units

- The Sen: 347 units

- Springleaf Residence: 941 units

- River Green: 524 units

Q8: How do current interest rates affect the Singapore property market?

A: Moderating interest rates in 2025 have made mortgages more affordable, potentially attracting investors back to the property market. This favourable interest rate environment also helps HDB upgraders afford private condominiums, assuming stable employment and real wages.

Q9: Is now a good time to invest in Singapore property?

A: The current market presents both opportunities and challenges. Positive factors include moderating interest rates, strong market fundamentals, and upcoming new launches providing more choices. However, investors should consider global economic uncertainties and US tariff policies that may affect buyer sentiment.

Q10: How does May 2025 compare to previous years without new launches?

A: Despite the monthly decline, May 2025’s sales performance (312 units excluding ECs) still outperformed other months over the past three years when no new projects were launched. The last time higher sales were recorded in a month without new launches was June 2022, before cooling measures were implemented.

Q11: What are Executive Condominiums (ECs) and why are they reported separately?

A: Executive Condominiums (ECs) are a hybrid housing type in Singapore that combines features of public and private housing. They are typically more affordable than private condominiums and have certain eligibility criteria. Property market reports often separate EC sales from private condominium sales to provide clearer market segmentation analysis.

Q12: What factors should property buyers consider in the current Singapore market?

A: Key considerations include:

- Interest rate trends: Monitor for potential changes affecting mortgage costs

- Project location: RCR projects showed the strongest performance

- Launch timing: Wait for upcoming launches for more choices

- Economic conditions: Consider global trade challenges and local employment stability

- Investment horizon: Long-term fundamentals remain strong despite short-term volatility

Disclaimer: The information provided here is for general guidance only. PropsBit.com.sg does not endorse or guarantee its suitability or accuracy for your specific situation. Although we strive to ensure the content is accurate and reliable at the time of publication, it should not substitute personalised advice from a qualified professional. We strongly recommend not relying solely on this information for financial, investment, property, or legal decisions, and we disclaim any responsibility for decisions made based on this content.

This website’s information is meant solely for general informational use. PropsBit.com.sg and its authors disclaim all liability and responsibility to any individuals or organisations for any outcomes resulting from the use of this website’s content or the information presented here. PropsBit.com.sg reserves the right to add, remove, or change the website’s content at any time without prior notice.