By Jim Tan · Licensed Singapore Property Agent · CEA Reg. No. R013675E · OrangeTee & Tie Pte Ltd · Published May 2026

The Singapore government has announced the most significant changes to the Executive Condominium (EC) housing scheme since 2013. Four rules have changed — and if you are an HDB upgrader planning to buy an EC, an existing EC owner, or someone who already signed an OTP for Rivelle Tampines or another recent EC, you need to understand exactly what this means for you.

Here is the short version:

✅ EC Minimum Occupation Period (MOP): doubled from 5 years to 10 years ✅ Deferred Payment Scheme (DPS) for new ECs: removed ✅ First-timer priority quota at EC launches: expanded ✅ Changes apply prospectively — existing EC buyers are almost certainly grandfathered

Let me break down each change, explain who is affected, and give you my honest assessment as a licensed Singapore property agent with 10+ years of transaction experience.

Why Did the Government Change the EC Rules?

The policy review was publicly committed to by Minister for National Development Chee Hong Tat during the Ministry of National Development Committee of Supply 2026 debate on 4 March 2026. The context was clear: EC prices had risen sharply, DPS take-up had climbed to a record 87.9% at Rivelle Tampines (from 71% at Aurelle of Tampines the year before), and the 5-year MOP was seen as enabling an “upgrade-and-flip” strategy that was inconsistent with the EC scheme’s original purpose of providing affordable home ownership for genuine upgraders.

Rivelle Tampines — which launched on 21 March 2026 and sold 92.5% of 572 units on launch day at an average of $1,893 psf — became the clearest evidence that the market needed recalibration. With 1,424 e-applications for 572 units (2.5x oversubscription) and the 30% second-timer quota exhausted by 2:15pm on launch day, the government acted decisively.

The official announcement came from MND/HDB. The authoritative text is available at HDB’s press releases page. Always verify the exact effective dates and wording there before making any financial commitment.

Change 1 — EC MOP Doubled from 5 Years to 10 Years

What changed

The Minimum Occupation Period for new ECs has been doubled from 5 years to 10 years, effective from the announced date. Under the previous rules, EC owners could sell on the open market to Singapore Citizens and PRs after 5 years. Under the new rules, that resale window opens only after 10 years — which also coincides with full privatisation (the point at which foreigners can buy).

In practice, this means the “buy EC at Year 0, sell to a Singaporean buyer at Year 5, recycle profits into a private condo” upgrade pathway that many second-timers have used — is now eliminated for new launches.

Who is affected — and who is NOT

This is the question everyone is asking. The government’s standard practice on property rule changes is to apply new restrictions prospectively — meaning they apply only to ECs where the Option-to-Purchase (OTP) is granted on or after the announced effective date.

If you have already exercised your OTP for Rivelle Tampines (March–April 2026), Aurelle of Tampines, Coastal Cabana, Tenet, Copen Grand, Lumina Grand, Altura, North Gaia, or any other EC launched before the announcement — you are almost certainly grandfathered under the original 5-year MOP.

I say “almost certainly” because the exact wording of the HDB press release determines the precise cut-off. It could be the OTP date, the developer’s application date, or the land tender award date. This distinction matters most for buyers who signed OTPs in the days immediately around the announcement. If you are in that window, check directly with HDB’s official press release or WhatsApp me at +65 9222-7288 for help interpreting your specific situation.

Summary table:

| EC Project | OTP Date | Likely MOP |

|---|---|---|

| Rivelle Tampines | March–April 2026 | ✅ 5 years (grandfathered) |

| Coastal Cabana | 2025 | ✅ 5 years |

| Aurelle of Tampines | 2025 | ✅ 5 years |

| Sora | 2024 | ✅ 5 years |

| North Gaia | 2022 | ✅ 5 years |

| Copen Grand | 2022 | ✅ 5 years |

| Tenet | 2022 | ✅ 5 years |

| Next new EC launch (Canberra Drive, Sembawang Drive, etc.) | After announcement | ❌ 10 years |

What this means for existing EC owners

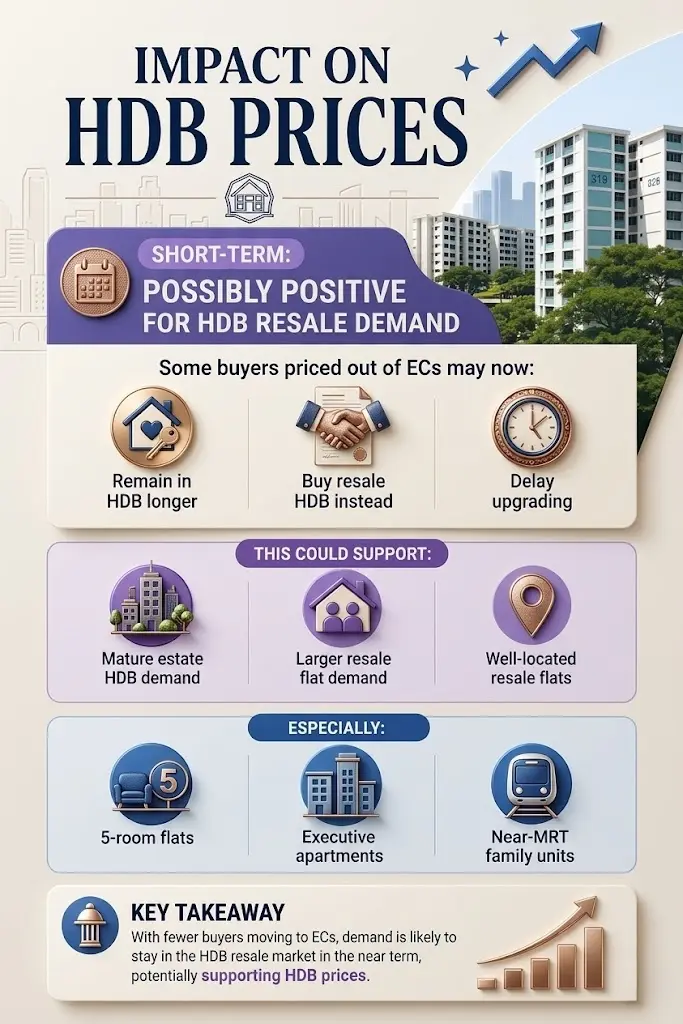

If you own an EC under the original 5-year MOP, you now hold a scarcity premium asset. Future EC buyers will be locked in for 10 years. Your EC — which can be resold to SC/PRs after just 5 years — will be structurally more liquid and more attractive in the resale market than any EC launched after the rule change.

The 11 ECs that privatised in 2026 (Citylife@Tampines, Lush Acres, Forestville and others) saw capital appreciation of 54.7% to 95.1% from their launch prices. The grandfathered cohort of 2022–2026 ECs is now even better positioned in the resale market, precisely because the new supply will carry a longer lock-in.

Change 2 — Deferred Payment Scheme (DPS) Removed for New ECs

What changed

The Deferred Payment Scheme — which allowed EC buyers to pay 20% upfront and defer the remaining loan repayments until TOP — has been removed for new EC launches going forward. New EC buyers must now service their mortgage under the Normal Progressive Payment Scheme (NPS) during construction.

This is a significant cashflow impact. Under DPS, an HDB upgrader could:

- Pay 5% cash + 15% CPF/cash as down payment

- Continue living in their HDB flat during construction

- Defer the bulk of loan repayments until TOP (~3–5 years later)

Under NPS (the reinstated default), progressive payments kick in at each construction milestone — foundation, structural frame, wall, windows, and so on — while the buyer is simultaneously paying for their existing HDB flat.

The cashflow reality without DPS

Here is a worked example for a $1.9 million EC (roughly in line with Tengah Garden Residences estimates):

| Phase | Amount Due | Timing |

|---|---|---|

| OTP booking fee (5% cash) | $95,000 | On signing |

| Exercise OTP (15% cash/CPF) | $285,000 | Within 8 weeks |

| Foundation complete (~10%) | $190,000 | ~Year 1 |

| Reinforced concrete (~10%) | $190,000 | ~Year 2 |

| Partition walls (~5%) | $95,000 | ~Year 2-3 |

| Windows (~5%) | $95,000 | ~Year 3 |

| TOP (~25%) | $475,000 | ~Year 4-5 |

| Legal completion (15%) | $285,000 | ~6 months post-TOP |

During construction, you will be paying progressive EC instalments while still paying for your HDB (either mortgage or rental if you have sold). Your MSR (Mortgage Servicing Ratio) is capped at 30% of gross monthly income — and this must be met during construction, not just at TOP.

Use my free TDSR Calculator and free Home Loan Affordability Calculator to model your exact numbers before committing. If the cashflow is tight, this is the conversation to have with me before signing anything.

Who is affected — and who is NOT

Rivelle Tampines buyers who used DPS are protected — their OTPs were exercised before the rule change. Rivelle is therefore very likely the last major Tampines EC where DPS was available at launch. This is an advantage Rivelle resellers can market after MOP.

All future EC launches from this point forward will be NPS only.

Change 3 — First-Timer Priority Quota Expanded

What changed

The historical EC launch structure was 70% first-timer quota / 30% second-timer quota, with the second-timer cap lifted one month after launch. The new rules expand the first-timer priority share — redirecting EC supply away from investors and repeat upgraders, and toward genuinely new household formations buying their first subsidised home.

The exact new percentage will be specified in the official HDB press release. Verify at hdb.gov.sg.

What this means for second-timers

If you are a second-timer (previously owned an HDB flat and are looking to buy a new EC), your ballot chances at launch are now smaller. You will face a longer wait for the second-timer window to open, and in a highly subscribed launch, you may not get a unit at all at launch pricing.

At Rivelle Tampines, the 30% second-timer quota (approximately 171 units) was fully exhausted by 2:15pm on launch day itself — suggesting the demand from second-timers already exceeded the quota. With a smaller second-timer allocation going forward, second-timers at popular EC launches will face even steeper odds.

What to do if you are a second-timer: Register your interest early, apply during the e-application window, and have a backup plan (a private condo in the same price range — like Tengah Garden Residences at $1,900–$2,100 psf estimated). WhatsApp me at +65 9222-7288 for a free eligibility review.

Who Remains Eligible to Buy a New EC in 2026?

The core eligibility rules are unchanged. To buy a new EC you must still:

✅ Be a Singapore Citizen (at least one applicant must be SC; co-applicant can be PR) ✅ Form an eligible family nucleus (married/fiancé scheme, public scheme, or orphan scheme) ✅ Have combined household income not exceeding $16,000/month ✅ Not own other private property locally or overseas, and not have disposed of any in the last 30 months ✅ Observe the 30-month wait-out period if previously owned private property

What has NOT changed:

- Income ceiling remains $16,000/month (under review per parliamentary remarks, but not changed yet)

- CPF Housing Grant: up to $30,000 for eligible first-timer SC/SC households

- MSR cap: 30% of gross monthly income

- TDSR: 55% of gross monthly income

- LTV: 75% maximum (bank loan), 5% minimum cash

- ABSD: Zero for eligible HDB upgraders purchasing first EC (HDB must be disposed within 6 months of TOP)

- Resale levy for second-timers: $15,000–$55,000 sliding by flat type — unchanged

Use my free Stamp Duty Calculator to model your full upfront costs including BSD.

Should I Still Buy a New EC in 2026?

My honest answer depends entirely on which buyer you are.

First-timer SC families — Yes, strongly

The case for ECs is still compelling for first-timers. You enter at approximately 20–25% below comparable private condo prices in the same area. You pay zero ABSD. You receive up to $30,000 CPF Housing Grant. The 10-year MOP is longer, but if you are buying to live in — not to flip — this is irrelevant to your daily life.

The next EC launches in the pipeline — Canberra Drive, Sembawang Drive, Woodlands Drive 17, Senja Close — will be the first under the new rules. Pricing may moderate slightly as DPS removal cools speculative demand, which could actually benefit genuine first-timer buyers with stronger balloting odds and potentially more competitive pricing.

HDB upgrader second-timers — Assess carefully

Without DPS, your cashflow commitment during construction is significantly higher. Without the 5-year MOP flip strategy, the investment thesis is fundamentally different — it is now a 10-year hold, not a 5-year one. If your finances can sustain progressive payments during construction alongside your HDB costs, and you are buying to live in for the long term, ECs still offer value. If you were banking on the flip-at-MOP strategy, that calculus has changed materially.

Investors — Private condo is now the clearer choice

The 10-year MOP and DPS removal both directly attack the EC investor use case. For buyers who want liquidity, capital appreciation, and flexibility — the $1,900–$2,100 psf range of an OCR private condo like Tengah Garden Residences or Vela Bay at $2,600–$2,800 psf now competes more directly with new ECs, without the lock-in constraints.

What This Means Specifically for Rivelle Tampines Buyers

If you bought at Rivelle Tampines EC — Singapore’s best-selling EC launch since 2017 — here is the specific impact:

MOP: Almost certainly grandfathered at 5 years from TOP (est. 2030), meaning you can resell from approximately 2035. Verify with HDB once you receive your official documentation.

DPS: Your DPS contract (if you used it — 87.9% of buyers did) is fully protected. Your payment schedule is unchanged.

Scarcity premium: Rivelle is now positioned as one of the last major ECs with 5-year MOP and DPS availability. In the resale market after 2035, this will be a distinguishing advantage vs ECs launched under the new 10-year MOP rules.

Bottom line: If you bought Rivelle Tampines at $1,893 psf average, you are holding a fundamentally sound asset with stronger liquidity characteristics than ECs launched from this point forward.

If you have specific questions about your unit or timeline, WhatsApp me directly at +65 9222-7288.

What Are the Next EC Launches in Singapore?

These are the EC sites expected to launch under the new rules:

| Project | Location | Expected |

|---|---|---|

| Canberra Drive EC | Sembawang, D27 | 2026 H2 |

| Sembawang Drive EC | Sembawang, D27 | 2026 H2 |

| Woodlands Drive 17 EC | Woodlands, D25 | 2027 |

| Senja Close EC | Bukit Panjang, D23 | 2027 |

These will be the first launches under the 10-year MOP and no-DPS regime. Expect developer GLS bid prices and launch PSF to be modestly lower as demand cools — particularly from second-timers and investors. Land cost for recent EC sites was approximately $794 psf ppr. Pricing is likely in the $1,950–$2,100 psf range.

Jim Tan’s Honest Assessment

Jim Tan is a licensed Singapore property agent (CEA Reg. No. R013675E) with OrangeTee & Tie Pte Ltd. He has transacted across HDB, resale condo, EC and new launch segments for over 10 years. Verify his CEA licence here.

My view: this policy change is sensible and long overdue. The EC scheme was designed to provide affordable home ownership for genuine middle-income Singaporeans — not to be a 5-year investment vehicle. The combination of record EC pricing ($1,893 psf at Rivelle vs $1,176 psf at Parc Central Residences in 2021), DPS take-up reaching 87.9%, and 2.5x oversubscription was exactly the kind of froth that justified intervention.

The critical point for current EC owners is this: the rule change validates your purchase. It signals that the government sees EC demand as genuine and worth protecting — not cooling by cutting supply, but by ensuring the scheme serves owner-occupiers rather than short-term investors. Your EC is now more scarce, not less valuable.

For buyers considering the next EC launches: the 10-year MOP fundamentally changes what an EC is. It is no longer a 5-year stepping stone. It is a 10-year family home commitment at a discount to private condos. If that matches your life plan, it still makes sense. If you were banking on flipping at MOP, look at private OCR condos instead — the entry price gap has narrowed but the flexibility is incomparable.

Before making any decision, use my free tools to run your numbers:

🧮 Free TDSR Calculator 🧮 Free MSR Calculator (30% cap applies to EC) 🧮 Free Stamp Duty Calculator (BSD + ABSD) 🧮 Free Home Loan Affordability Calculator 🧮 Free Progressive Payment Calculator

Frequently Asked Questions — Singapore New EC Rules 2026

Is the new 10-year EC MOP retroactive? Does it apply to Rivelle Tampines buyers? Based on Singapore’s standard approach to property rule changes, the 10-year MOP applies prospectively — to ECs where the OTP is granted on or after the effective date of the announcement. Buyers who already exercised their OTP for Rivelle Tampines (March–April 2026) or any earlier EC are almost certainly grandfathered under the original 5-year MOP. Verify the exact cut-off date in the official HDB press release at hdb.gov.sg, or WhatsApp Jim at +65 9222-7288 for guidance on your specific situation.

Can I still use DPS for my Rivelle Tampines EC purchase? Yes. If you signed your OTP and exercised DPS before the rule change was announced, your Deferred Payment Scheme contract is fully protected. The removal of DPS applies only to new EC launches going forward. Rivelle Tampines is almost certainly the last major Tampines EC where DPS was available, which is a resale advantage for Rivelle owners after MOP.

What is the new first-timer quota for EC in Singapore? The exact new first-timer quota percentage will be specified in the official MND/HDB press release. The previous structure was 70% first-timer / 30% second-timer at launch. The announcement expands first-timer priority. Check the official HDB press release for the precise numbers.

Does the EC income ceiling of $16,000/month still apply? Yes, the $16,000/month combined household income ceiling is unchanged by this announcement. It remains under active review per Minister Chee Hong Tat’s Parliamentary remarks, but no change has been announced. If your income exceeds $16,000/month, you are not eligible for a new EC and should consider private condos like Tengah Garden Residences or Vela Bay.

Am I still eligible for the $30,000 CPF Housing Grant for my EC? Yes — the CPF Housing Grant for new ECs is unchanged. First-timer SC/SC households earning up to $10,000/month are eligible for up to $30,000. The grant decreases on a sliding scale between $10,001–$12,000/month and is zero above $12,000/month. Note that the grant is funded by CPF and applied to your purchase price, not paid in cash.

Should HDB upgraders still buy a new EC after the 10-year MOP change? It depends on your purpose. If you are buying an EC to live in for the long term as a family home — the EC is still excellent value at approximately 20–25% below comparable private condos, with no ABSD and CPF Grant available. If you were planning to sell at the 5-year MOP and upgrade to private, that strategy no longer works for new EC launches. In that case, a private condo in the OCR (like Tengah Garden Residences at est. $1,900–$2,100 psf) may be the better choice. WhatsApp Jim at +65 9222-7288 for a personalised assessment.

Will EC prices fall after the new rules? Likely to moderate somewhat — particularly at launch. DPS removal eliminates the 3% price premium that DPS buyers absorbed, and reduced second-timer demand should reduce oversubscription. However, the underlying driver of EC demand — a large cohort of HDB upgraders with growing incomes and genuine housing needs — is unchanged. A modest correction from the $1,893 psf Rivelle peak is possible; a collapse is not supported by fundamentals.

What is the difference between EC MOP and EC privatisation? Under the original rules: EC MOP was 5 years (can sell to SC/PR after Year 5), full privatisation at Year 10 (can sell to foreigners). Under the new rules: both milestones coincide at Year 10 — you can sell to SC/PR and to foreigners at the same time, after a single 10-year lock-in period. This is a meaningful simplification of the EC structure.

Do the new EC rules affect my ability to rent out my EC unit? During the MOP (whether 5 or 10 years), you cannot rent out the entire EC unit. You may rent out individual rooms subject to conditions. After MOP, you can rent the whole unit freely. The 10-year MOP doubles the period during which whole-unit rental is not permitted — a cashflow consideration for buyers who intended to rent out their EC after the original 5-year MOP.

What are the next EC launches in Singapore after the rule change? The next EC launches expected are Canberra Drive EC and Sembawang Drive EC (both D27, Sembawang area, expected H2 2026), Woodlands Drive 17 EC (D25, 2027) and Senja Close EC (D23 Bukit Panjang, 2027). These will be the first launches under the 10-year MOP and no-DPS regime. Register your interest early — WhatsApp Jim at +65 9222-7288 to be notified.

Explore Related Projects

→ Rivelle Tampines EC — 92.5% sold, limited bounced units available (D18) → Tengah Garden Residences — First private condo in Tengah Forest Town, est. $1,900–$2,100 psf (D24) → Vela Bay — First private condo in Bayshore precinct, est. $2,600–$2,800 psf (D16) → One Marina Gardens — First private condo in Marina South, from $2,343 psf (D1) → Free TDSR Calculator — Check your EC loan eligibility → Free Stamp Duty Calculator — Calculate your exact BSD and ABSD

Talk to Jim — Free, No Hard Selling

Whether you bought an EC recently and want to understand how the new rules affect you, or you are planning to buy one of the next launches — I will give you honest, personalised advice based on your actual financial situation.

💬 WhatsApp Jim at +65 9222-7288 📅 Book a free consultation at propsbit.com.sg/contact/

Jim Tan · CEA Reg. No. R013675E · OrangeTee & Tie Pte Ltd (Agency Licence L3009250K) Verify Jim’s CEA licence →

Disclaimer: All information in this article is based on publicly available reporting and the official announcement from MND/HDB. Always verify the exact effective dates, wording, and grandfathering conditions in the official HDB press release at hdb.gov.sg before making any financial commitment. This article is for general information only and does not constitute legal or financial advice. Jim Tan (CEA R013675E), OrangeTee & Tie Pte Ltd (L3009250K), regulated by the Council for Estate Agencies Singapore.