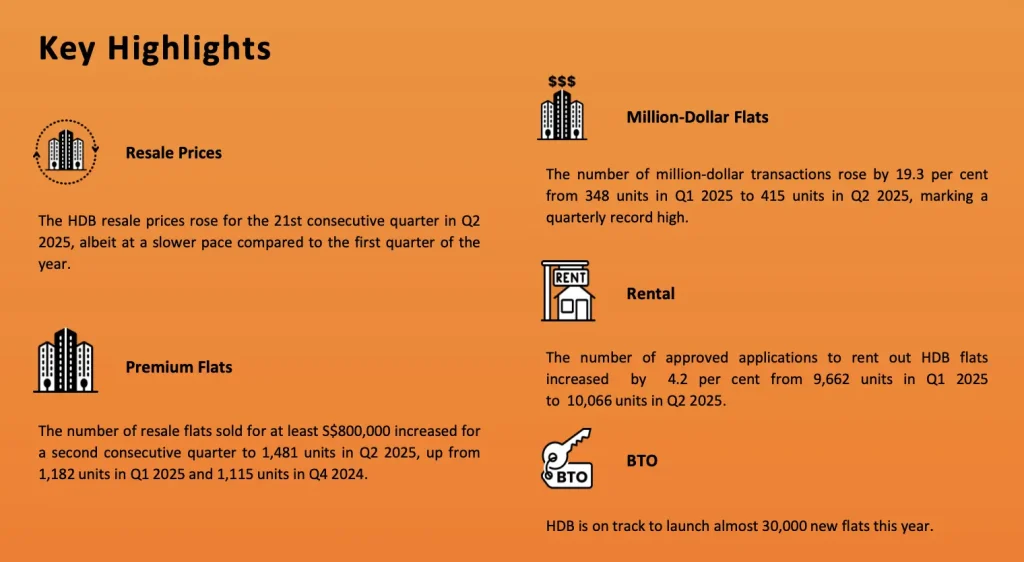

The Singapore HDB resale market achieved a historic milestone in Q2 2025, recording 21 consecutive quarters of price growth – the longest streak ever recorded in Singapore’s public housing history. Despite this remarkable achievement, the market showed signs of moderation with the slowest quarterly growth rate since Q2 2020 at just 0.9%.

Key Market Performance Indicators Q2 2025

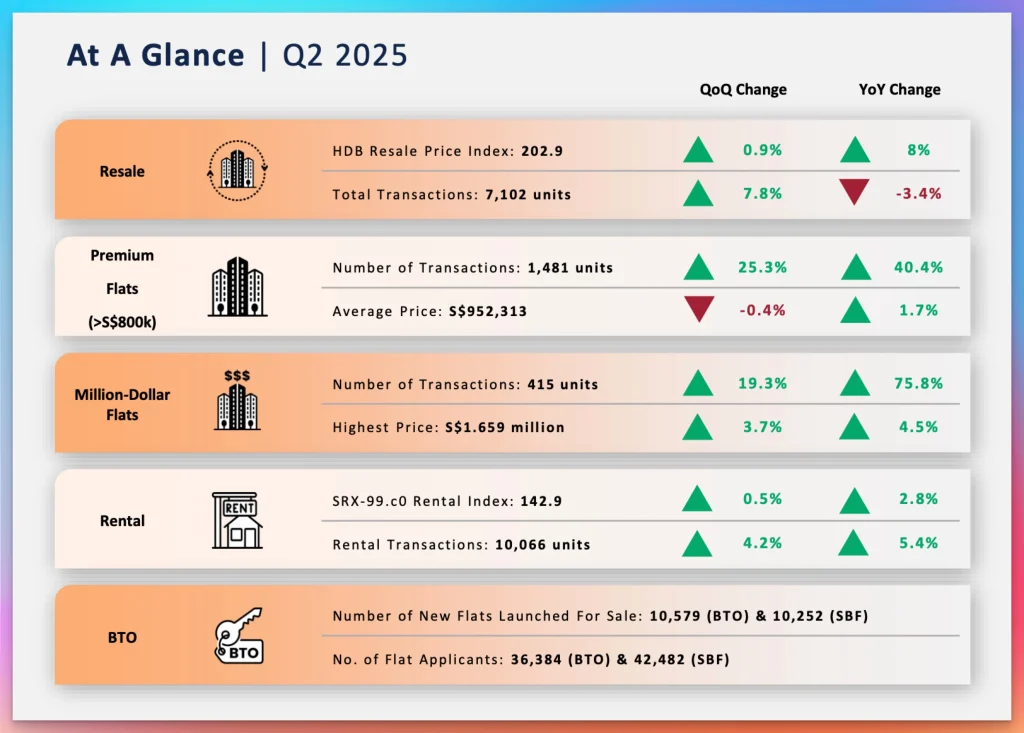

HDB Resale Price Index reached 202.9, representing 0.9% quarterly growth (slowest since Q2 2020)

Total resale transactions increased 7.8% to 7,102 units from 6,590 units in Q1 2025

Premium flats (≥$800,000) surged 25.3% to 1,481 units, marking the second consecutive quarterly increase

Million-dollar flats hit record quarterly high with 415 transactions (+19.3% from Q1)

Most expensive transaction: $1.659 million premium apartment loft at Dawson Road

HDB rental volume increased 4.2% to 10,066 approved applications

Historic Price Growth Achievement vs Market Cooling

Unprecedented 21-Quarter Growth Streak

Q2 2025 marks the longest price growth streak ever recorded. Prices have grown continuously for 21 consecutive quarters from Q1 2020 to Q2 2025, compared to the 20 consecutive quarters of increase from Q4 1991 to Q4 1996. This historic achievement demonstrates the resilience of Singapore’s public housing market despite global economic uncertainties.

Historical Context:

Current streak (Q1 2020 – Q2 2025): 21 quarters, 54.3% total growth

Previous record (Q4 1991 – Q4 1996): 20 quarters, 294.4% total growth

Growth pace: Current increases are more sustainable compared to the dramatic 1990s surge

Cooling Price Momentum Signals Market Maturation

The 0.9% quarterly growth in Q2 2025 represents the third consecutive slowdown, declining from:

Q4 2024: Higher growth momentum

Q1 2025: 1.6% quarterly increase

Q2 2025: 0.9% quarterly increase (current)

Annual Perspective:

H1 2025 growth: 2.5% (vs 4.2% in H1 2024, matching 2.5% in H1 2023)

Year-on-year Q2 comparison: Lower than 2.3% recorded in Q2 2024

The million-dollar HDB segment achieved unprecedented heights with 415 transactions in Q2 2025, representing a 19.3% quarterly increase from 348 units in Q1 2025. This performance sets a new quarterly record and positions 2025 to potentially exceed the 2024 full-year record of 1,035 units.

2025 Performance Trajectory:

H1 2025: 763 million-dollar transactions

Annual projection: On track to exceed 1,035 units (2024 record)

Growth momentum: Consistent quarterly increases

Premium Transaction Highlights

Record-Setting Sale:

Address: Dawson Road premium apartment loft

Size: 122 sqm (1,313 sqft)

Price: $1,658,888

Significance: Highest Q2 2025 transaction

Geographic Distribution of Million-Dollar Flats: Million-dollar transactions were concentrated in premium locations with excellent connectivity and established amenities, reflecting buyer preference for prime locations despite premium pricing.

Market Dynamics Supporting Million-Dollar Growth

Supply Constraints:

Limited large flat availability in prime locations

Private property owners potentially benefiting from a 15-month wait-out period review

Cash-rich buyers from private property sales

Premium HDB Flats (≥$800,000) Market Surge

Strong Demand Across Price Segments

The number of resale flats sold for at least S$800,000 increased for a second consecutive quarter to 1,481 units in Q2 2025, up from 1,182 units in Q1 2025 and 1,115 units in Q4 2024.

Growth Metrics:

Quarterly increase: +25.3% (1,481 vs 1,182 units)

Year-on-year growth: +40.4% (1,481 vs 1,055 units)

Trend duration: Second consecutive quarterly increase

Top Towns for Premium Transactions (≥$800,000)

Leading Premium Markets:

Tampines: 150 units (volume leader)

Toa Payoh: 138 units (central location premium)

Bukit Merah: 129 units (city fringe appeal)

Kallang/Whampoa: 97 units (urban regeneration benefits)

The HDB rental market demonstrated healthy fundamentals with 10,066 approved rental applications in Q2 2025, representing a 4.2% increase from 9,662 applications in Q1 2025.

Rental Market Dynamics:

Seasonal strength: Q2 typically shows higher rental activity

Price growth: Modest 0.5% increase (vs 0.1% in Q1 2025)

SRX-99.co HDB Rental Index: 142.9

Year-on-year outlook: Stable growth trajectory

Competitive Landscape Impact

Private Market Competition:

Many new condominium completions are increasing the rental supply

Private landlords are reducing asking rents due to macroeconomic uncertainties

Tenant migration from HDB to the private rental market

Result: Moderated HDB rental growth expectations

Annual Projections:

Rental price growth: 1-2% for the full year 2025

Rental volume estimate: 37,000-38,500 units annually

BTO and SBF Market Analysis 2025

Near-Record New Flat Supply

HDB is on track to launch almost 30,000 new flats this year, comprising over 19,000 BTO flats and more than 10,000 flats under the Sale of Balance Flats.

Supply Breakdown:

BTO flats: Over 19,000 units planned

Sale of Balance Flats: Over 10,000 units

Total 2025 supply: Nearly 30,000 units

Historical context: Significant supply increase

July 2025 BTO Launch Analysis

New Project Details:

Total projects: 8 developments

Total units: 5,547 flats

Coverage: 7 towns across Singapore

Featured locations: Bukit Merah, Bukit Panjang, Clementi, Sembawang, Tampines, Toa Payoh, Woodlands

Policy Innovation – Deferred Income Assessment:

New rule: Only one party in a couple needs a student/NS status

Impact: More couples eligible for deferred assessment

Expected outcome: Increased applications for larger/premium units

Sale of Balance Flats Record Supply

2025 SBF Performance:

February 2025: 5,590 units released

July 2025: 4,662 units offered

Total H1 2025: 10,252 SBF units

Historical significance: Highest annual SBF supply on record (previous high: ~10,200 units in 2016)

Application Demand Analysis

High-Demand Projects:

Tampines: Strategic location, MRT connectivity

Toa Payoh: Central location, established amenities

Income ceiling for BTO applications: Potential increase

Minimum age for singles: Current 35-year threshold under review

15-month wait-out period: Possible removal for private property owners

VERS (Voluntary Early Redevelopment Scheme): Launch in the early 2030s

Expected Market Effects:

Higher income ceiling: More BTO applications, reduced resale pressure

Lower age requirement: Expanded buyer base

Wait-out period removal: Premium segment demand increase

VERS program: Lease decay concern mitigation

Geographic Growth Areas

Master Plan 2025 Beneficiaries: Areas expected to experience increased interest due to planned developments:

Bishan: Community hub developments

Dover: Infrastructure improvements

Sengkang: Continued expansion

Woodlands: Northern gateway development

Yio Chu Kang: Transportation and amenity upgrades

Investment Strategy Implications

Market Positioning Recommendations:

For Value Investors:

Focus areas: Woodlands, Yishun, Jurong West

Strategy: Long-term appreciation potential

Risk profile: Moderate, steady growth expected

For Premium Investors:

Target locations: Central Area, Bishan, Queenstown

Strategy: Scarcity play, established demand

Risk profile: Higher entry cost, established value retention

For Rental Investors:

Optimal areas: Near MRT stations, established towns

Strategy: Steady rental yield focus

Market conditions: Competitive but stable

Risk Factors and Market Considerations

Supply-Side Pressures

Increased Competition:

Nearly 30,000 new flats are launching in 2025

Higher BTO and SBF supply creates alternatives

Potential buyer shifts from resale to new flats

Policy Uncertainties:

Income ceiling and age requirement reviews

Wait-out period potential removal

Market structure changes are possible

Economic Environment

Supporting Factors:

Declining interest rates are improving affordability

Stable economic fundamentals

Continued population growth

Risk Factors:

Global economic uncertainties

Geopolitical tensions affecting sentiment

Macroeconomic policy changes

HDB Resale Market Projection

Indicators

2022

2023

2024

Q1 2025

Q2 2025

1H 2025

Projection for 2025

Price Index (Price Change)

10.4%

4.9%

9.7%

1.6%

0.9%

2.5%

4% to 5.5%

Sales Volume (units)

27,896

26,735

28,986

6,590

7,102

13,692

27,000 to 28,000

Rental Price Change (SRX-99.co)

28.5%

10.2%

3.6%

0.1%

0.5%

0.6%

1% to 2%

HDB Rental Applications

36,166

39,138

36,673

9,662

10,066

19,728

37,000 to 38,500

Source: HDB, SRX-99.co, Realion Research

Frequently Asked Questions Singapore HDB Market

Why did HDB price growth slow to 0.9% in Q2 2025?

The slowdown reflects increased new flat supply (nearly 30,000 units launched in 2025), seasonal factors including June school holidays affecting buyer activity, and market maturation after 21 consecutive quarters of growth.

Are million-dollar HDB flats still a good investment?

With 415 million-dollar transactions in Q2 2025 (record quarterly high), these properties continue showing strong demand. However, buyers should consider location premiums, replacement costs, and long-term demographic trends.

Which HDB towns offer the best value in Q2 2025?

Based on price growth and transaction volumes, Yishun, Woodlands, and Jurong West offer value positioning, while Punggol and Sengkang provide balanced growth with modern amenities.

How will increased BTO supply affect resale prices?

The nearly 30,000 new flats launching in 2025 may moderate resale price growth by providing alternatives to buyers, potentially leading to more sustainable 4-5.5% annual price appreciation rather than double-digit growth.

Should I buy HDB resale now or wait for more BTO launches?

Consider your timeline needs, budget constraints, and location preferences. Resale offers immediate availability but at current market prices, while BTO provides value but requires waiting periods and location limitations.

About PropsBit.com.sg

PropsBit.com.sg delivers comprehensive Singapore HDB market analysis, resale insights, and investment guidance across all towns and flat types. Our experienced OrangeTee & Tie agents provide personalised strategies for HDB buyers, sellers, and investors navigating Singapore’s dynamic public housing market.

Consult our HDB specialists for town-specific insights, investment strategies, and access to exclusive resale opportunities tailored to your housing and investment objectives.

Disclaimer: Property investments carry risks. HDB eligibility rules apply. Past performance does not guarantee future returns. Consult qualified professionals before making property decisions.

Newsletter Updates

Enter your email address below and subscribe to our newsletter