Let's Shape The Future Of Your Investments!

Natoque iaculis cursus augue urna commodo aptent morbi tortor porttitor quis ornare.

Understanding TDSR: Your Comprehensive Guide to Total Debt Servicing Ratio. Introduced in Singapore, the Total Debt Servicing Ratio (TDSR) is a critical financial metric that plays a significant role in the loan application process for individuals seeking to take on debt in Singapore.

This article delves into the intricacies of TDSR, explaining its importance, how it is calculated, and its implications for various types of loans, including personal and property loans.

Understanding TDSR is essential for anyone looking to manage their debt responsibly, ensuring they do not overextend themselves financially.

This guide will equip you with the knowledge to navigate the complexities of borrowing in Singapore, making it a must-read for potential borrowers.

TDSR plays a crucial role in maintaining financial stability within Singapore’s economy. By regulating how much debt individuals can take on relative to their income, it helps prevent situations where borrowers commit to debt levels that exceed their repayment capabilities.

This is particularly important given the rising property prices and increasing living costs in Singapore. Additionally, understanding your TDSR can empower you as a borrower.

It enables you to make informed decisions about your finances, ensuring that you do not overextend yourself when applying for loans.

A well-managed TDSR can also improve your chances of loan approval, as lenders will view you as a lower-risk borrower.

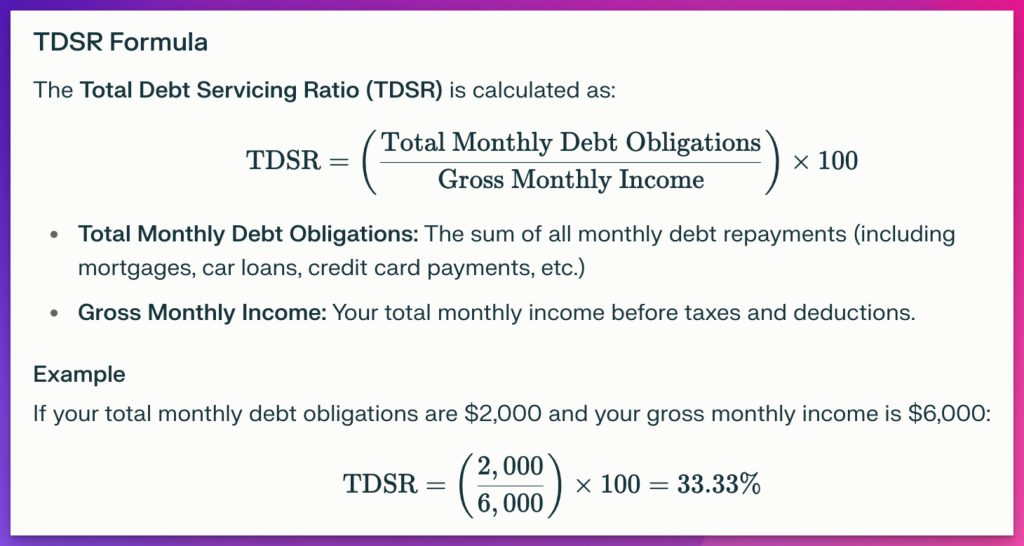

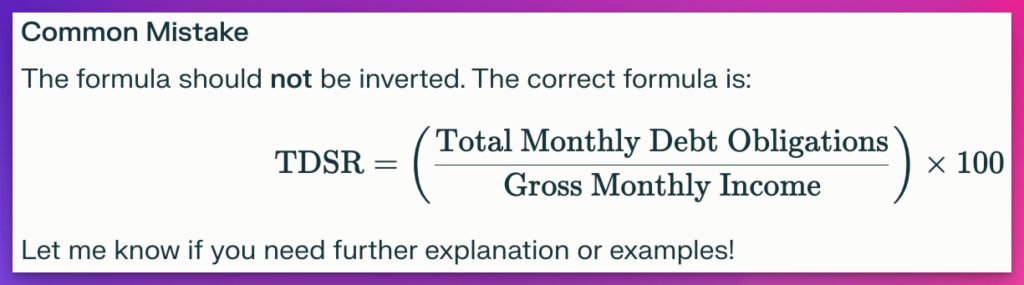

Calculating your Total Debt Servicing Ratio involves dividing your total monthly debt obligations by your gross monthly income.

The formula can be expressed as:

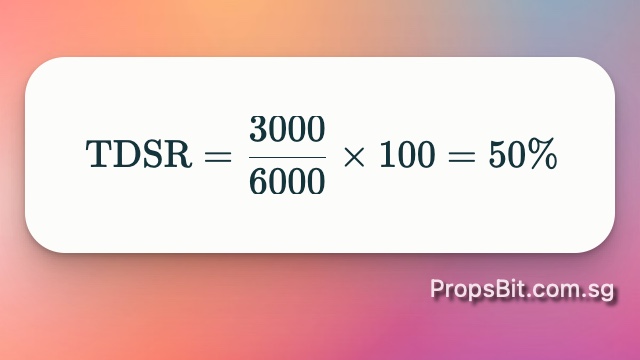

For example, if your total monthly debt obligations amount to SGD 3,000 and your gross monthly income is SGD 6,000, your TDSR would be:

This calculation illustrates how much of your income goes towards servicing your debts. It’s essential for potential borrowers to keep track of their existing debts and ensure they remain within the acceptable limits set by financial institutions.

The rules governing the Total Debt Servicing Ratio are designed to protect both borrowers and lenders. Here are some key aspects:

These rules ensure that borrowers do not take on excessive debt relative to their income levels, fostering a more sustainable borrowing environment.

When applying for a loan in Singapore, lenders will assess your TDSR as part of their evaluation process. A lower TDSR indicates that you have more disposable income available after servicing existing debts, making you a more attractive candidate for new loans.

If your calculated TDSR exceeds 55%, lenders may either decline your application or offer you a smaller loan amount than requested. This could significantly impact your plans if you were relying on that loan for significant purchases like property or vehicles.

Additionally, understanding how lenders view your TDSR can help you strategise your loan applications effectively. For instance, paying down existing debts before applying for new financing can improve your ratio and increase your chances of approval.

The Total Debt Servicing Ratio applies to various types of loans in Singapore:

Understanding how different types of loans contribute to your overall debt picture can help you

manage them effectively while keeping within acceptable limits set by the MAS.

While both Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR) serve as measures for assessing borrowing capacity, they focus on different aspects:

| Feature | Total Debt Servicing Ratio (TDSR) | Mortgage Servicing Ratio (MSR) |

|---|---|---|

| Definition | Measures total monthly debt obligations against gross income | Measures only housing-related debts against gross income |

| Applicability | Applies to all types of loans | Specifically applies to housing loans |

| Limit | Maximum 55% | Maximum 30% |

The MSR is particularly relevant for those seeking home financing as it ensures that borrowers do not overcommit themselves solely based on housing expenses.

Understanding both ratios can provide comprehensive insights into managing overall financial health.

Improving your Total Debt Servicing Ratio involves strategic financial planning and management:

By actively managing these factors, you can improve your financial standing and create a healthier

borrowing profile.

Certain exemptions exist within the framework of the Total Debt Servicing Ratio rules:

Understanding these exemptions can provide opportunities for borrowers who might otherwise

struggle with strict adherence to standard guidelines.

Debt obligations encompass all recurring payments that affect an individual’s financial profile:

Being aware of what constitutes total debt obligations helps borrowers manage their finances

better and stay within acceptable limits when applying for new credit facilities.

The Loan-to-Value ratio (LTV) measures how much loan you are taking out compared to the value of the property being purchased:

A higher LTV indicates higher risk for lenders since it suggests less equity in the property being financed. LTV ratios often influence both mortgage approval processes and interest rates offered by lenders.

Maintaining an appropriate LTV ratio alongside managing a healthy Total Debt Servicing Ratio ensures responsible borrowing practices while maximising financing opportunities.

Interest rates play a significant role in determining monthly repayment amounts:

Understanding how interest rates affect overall debt obligations allows borrowers to make

informed choices regarding loan products that align with their financial goals without exceeding

acceptable thresholds set by regulatory bodies like MAS.

Exceeding the Total Debt Servicing Ratio limit can have serious implications:

Being proactive about managing debts ensures compliance with established guidelines while

safeguarding future borrowing capabilities essential for achieving long-term financial objectives

effectively.

When applying for personal loans in Singapore:

For those seeking property financing:

Understanding TDSR can help you make informed decisions about borrowing:

In conclusion, mastering the concept of TDSR is essential for anyone looking to borrow in Singapore. By understanding how it works and how to optimize your financial position, you can navigate the loan application process more effectively and increase your chances of approval.Key takeaways:

Remember, responsible borrowing is key to maintaining financial health. Always assess your ability to repay before taking on any new debt obligations.

Understanding Total Debt Servicing Ratios is essential for responsible borrowing practices in

Singapore’s competitive financial landscape:

In Summary:

By following these principles diligently, individuals position themselves favourably within dynamic economic environments while pursuing long-term aspirations without compromising fiscal stability!

A: The Total Debt Servicing Ratio (TDSR) is a framework introduced by the Monetary Authority of Singapore to ensure borrowers don’t over-extend themselves when taking on property loans. It limits the amount that individuals can borrow based on their total debt obligations and income. The TDSR applies to both residential and investment property loans in Singapore.

A: The TDSR will be calculated based on the borrower’s total monthly debt obligations divided by their gross monthly income. The total debt obligations include all outstanding loans, including the new property loan being applied for. The TDSR must not exceed 55% of the borrower’s gross monthly income.

A: While both TDSR and MSR (Mortgage Servicing Ratio) are debt servicing frameworks, they apply to different scenarios. The TDSR applies to all property loans, including private properties and investment properties. The MSR, on the other hand, only applies to loans for HDB flats and executive condominiums. The MSR limits housing loan payments to 30% of a borrower’s gross monthly income.

A: The TDSR limits the amount you can borrow for a property based on your income and existing debts. If your total debt obligations exceed 55% of your gross monthly income, you may need to reduce your loan amount, extend your loan tenure, or increase your down payment to meet the TDSR requirements.

A: Yes, there are some situations where borrowers may be exempted from the TDSR framework. These include refinancing of owner-occupied properties, loans for owner-occupied properties that don’t exceed a certain Loan-to-Value ratio, and some specific scenarios involving investment properties. However, these exemptions are subject to certain conditions and may change over time.

A: While the TDSR doesn’t directly affect interest rates, it can influence the type of home loan you’re eligible for. If you’re close to the TDSR limit, you might have fewer options for loans, which could potentially impact the interest rate you’re offered. It’s always best to shop around and compare different bank loans to find the most competitive interest rate.

A: Generally, banks are required to maintain a TDSR of 55% or less for borrowers. However, in some cases, banks may have some flexibility for borrowers with high net worth or financial buffers. It’s best to consult with financial advisors or mortgage specialists to explore your options if your TDSR exceeds 55%.

A: To improve your TDSR and potentially qualify for a larger property loan, you can consider several strategies: increasing your income, reducing your existing debts, extending your loan tenure (which reduces monthly payments), or making a larger down payment. Remember, the goal is to ensure your total monthly debt obligations don’t exceed 55% of your gross monthly income.

Disclaimer: This information is provided for informational purposes only. PropsBit.com.sg does not endorse or guarantee its relevance or accuracy concerning your situation. While careful efforts have been taken to ensure the content’s correctness and reliability at the time of publication, it should not replace personalised advice from a qualified professional. We highly recommend against relying solely on this information for financial, investment, property, or legal decisions, and we accept no responsibility for choices made based on this content.